APRIL 2019 WALNUT MONTHLY MANAGEMENT REPORT AND DISCUSSION

MMR APR2019

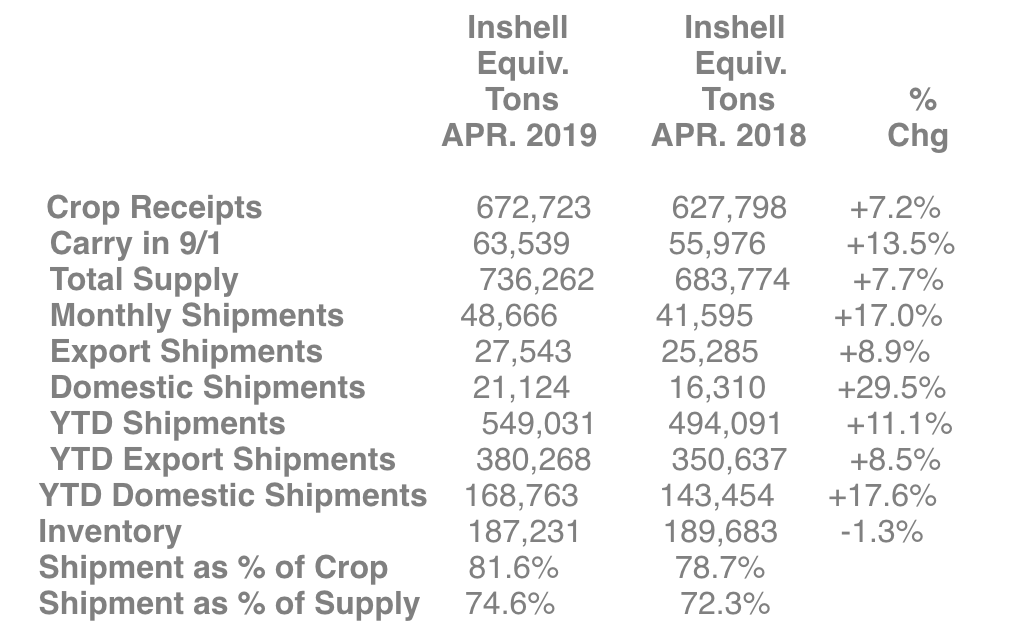

The California Walnut Board released the APRIL 2019 Position Report. Our table of these figures are shown below:

MMR and YTD HIGHLIGHTS

1) Monthly inshell equivalent shipments up 17% vs PY

- Export inshell equivalent shipments up 8.9% vs PY

- Domestic inshell equivalent shipments up 29.5%

2) Year to date inshell equivalent shipments now up 11.1% vs PY

- Export inshell equivalent YTD shipments up 8.5% vs. PY

- Domestic inshell equivalent YTD shipments up 17.6% vs. PY

MMR DISCUSSION

The Calif. Walnut industry had a surprisingly strong April 2019 up 17% over PY April 2018. The industry was braced for a moderate if not mediocre report as most packers felt to be "quiet" but this performance was very strong.

This performance comes on the heels of a strong March 2019 which was up 26.3% over PY, February 2019 which was up 35.9% over PY and a January 2019 up 38.7% against PY. Year to date April 2019 shipments are up 11.1% vs. PY with Export up 8.5% and domestic up 17.6% vs. PY. All very strong numbers.

April 2019's strong performance is due to:

- Strong USA kernel shipments up 31.7% over PY April 2019. Many believe that April's shipment of 18.4 million pounds is bolstered by two prior USDA trade mitigation buys which are mostly likely shipping and will continue to ship in the coming months. If this in fact is the case, the US Walnut industry might already have a solid amount of sales for May, June, July and August due to these trade mitigation buys.

- Strong European kernel shipments up 31.33% over PY April 2019 mostly help by Germany's 64% increase.

- Good Kernel shipments to the Middle east/Africa up 26.79% over PY 2019

- Total April 2019 Domestic kernel shipments up 31.7% with Export Kernel up 6.2% and Export Inshell up 33%.

Analytical Discussion

Following last month's presentation of the below historical table, we've added performance for April 2019. With this, the industry is at 81.3% sold based on "crop". Assuming the next 4 months performance in red, the industry could conceivable sell 101.4% of the crop thus cutting into to the carryout (which we assumed would be equivalent to the carry in of 63,539 ton).

Calif. Walnuts Shipments by Month, Inshell equivalent ton

The chart above suggest that for the next 4 months, May 2019 - August 2019, the industry needs to average 33,750 ton of sales each month to move 101.4% of the crop leaving slightly less than the 2018 "carry in" of 63,539 ton amount as the 2019 "carry out". While this seems reasonable, the quietness on a spot basis is deafening quite possibly due to the USDA trade mitigation program which might "mask" the slow down otherwise. Also, while some packers are very well sold, there are other packers with significant inventory at present that they are inquiring us to move every day, albeit at full market prices. When will this product get moved?

Other considerations

- Chile - On 7th of May at the Chilenut meeting, Chile revised their crop down to 130,000 tons from 150,000 tons. This shocking news comes in after a crop receipt survey conducted by Chilenut members on 1st week of May indicating that Serr is down by 20% and Chandler is down by 15%. Sale commitments reported by Chilenut members is at 65% which 70% is inshell and 50% kernel. Chilean inshell shipments for March and April were around 18,000 ton compared to 14,000 tons last year, up by 28%. This is not a total surprise considering last year Chile started the season with inshell Chandler at $4.20/kg and this season with a 37% lower price at $2.65/kg CFR. Kernel shipments for March and April were around 800 tons. Chilean authorities are currently in discussion with the Indian authorities to lower the tariffs on walnuts to around 50%. At this stage nothing is certain as to when this will happen or how much the tariffs will be lowered by. Current price of inshell Chandler is at $2.70-2.75/kg CFR and 80% LHP at $7.10/kg ($3.22/lb). Depending on quality Hand Cracked is between $9.00 and $11.00/kg CFR. It seems that Chile is well sold with inshell, will kernel sales catch up? Does Chile need to come back to the market and sell their remaining stock as inshell? Will the stock pile situation in Dubai disappear anytime soon? How will this affect the first containers of Chilean walnuts arriving at their destination? What will it mean for Chile when USA starts offering new crop at INC next week?

- Cold Storage - This is clearly in full force. Some good deals can be had at present.

- New Crop - There has been some discussion in the field by packers and growers notating "not many nut clusters as triples and quadruples and more singles and doubles". While still too early to tell, could this be a more definitive talking point in the future? With this, some packers have talked about the new crop 2019 being closer to this current crop of 672,723 ton instead of something over 700,000 ton.

- Pricing or walnut material is as follows has changed very little from last month: Domestic LHP $2.60 -$2.85/lb, Export quality 20% LHP $2.95 - $3.10/lb. CHP $2.40/lb to $2.50/lb. Chandler Halves $3.30 to $3.50/lb range with minimal material available. Inshell material is pretty much non-existent.

Conclusion - The historical chart still suggests that the industry is in a good position. With the strong April, the average sales figure of 33,750 inshell ton seams reasonable and California seems to be on pace to oversell the crop and reduce the carry-out number to below that of the carry-in number. There are some good deals on Domestic LHP and CHP on a nearby spot basis but still only minimal amounts of Chandler LHP or Chandler Halves available.